Electronic warfare market accelerates

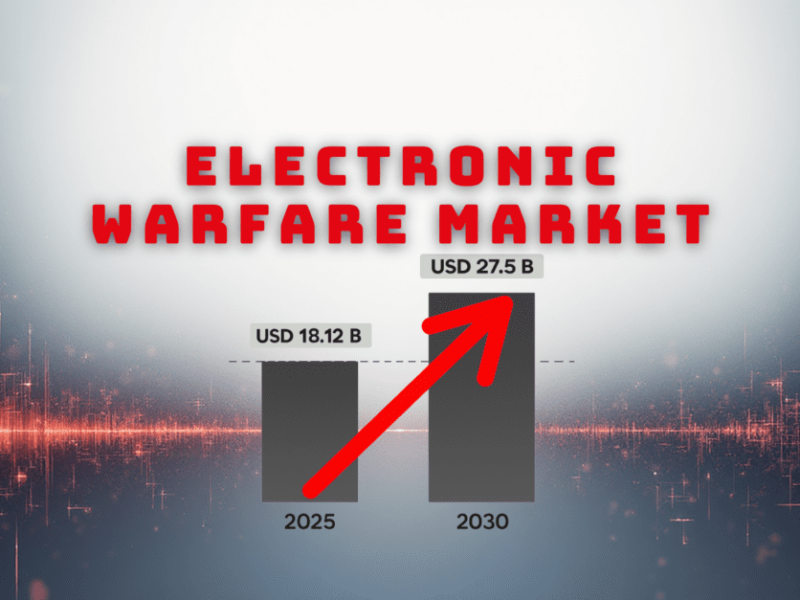

The global electronic warfare (EW) sector is entering a renewed growth cycle. Mordor Intelligence is forecasting growth from $18.12 billion in 2025 to $27.50 billion by 2030.

Rising geopolitical tensions and rapid advances in signal-interference technologies are reshaping priorities across defense programs worldwide. For eeNews Europe readers, the report highlights key semiconductor, RF, and system-integration trends that will influence design roadmaps, procurement opportunities, and competitive positioning across the European defense electronics supply chain.

Space-based EW, software-defined architectures

Mordor Intelligence identifies a surge of investment in space-based EW constellations as nations look for new vantage points to counter long-range missile systems, satellite communications, and electronic-intelligence operations. While airborne platforms still dominate spending, emerging requirements increasingly favor directed-energy weapons, agile counter-UAS systems, and software-defined architectures that can adapt in real time.

Europe and North America are seeing a wave of reshoring activity as supply-chain disruptions and tighter export controls on semiconductor materials pressure governments and primes to reduce reliance on overseas gallium-based component sources. This transition is reshaping competition, opening the door to smaller firms offering modular, software-first EW systems.

Combatting evolving signal and radar threats

As radar and communications signals become more agile, modern defense networks face an environment where traditional jamming techniques are losing effectiveness. The report notes that defense agencies are turning to machine learning to identify unfamiliar emitters more quickly and to automate countermeasures.

Quantum radar research adds further urgency, motivating investment in advanced decoys, signature management, and memory-based signal replication. The integration of 5G and early-stage 6G technologies is also complicating the EW landscape, driving demand for flexible, upgradable solutions that can be remotely reconfigured.

Unmanned systems take on a central EW role

Unmanned aerial systems (UAS) are now considered essential EW assets, with modular payloads capable of disrupting enemy networks in real time. Thanks to advances in compact, high-power semiconductor devices, even small drones can now deploy jamming systems previously limited to large aircraft.

The rise of teaming concepts—pairing autonomous drones with piloted fighters—has accelerated interest in next-generation onboard protection and eelectronic-defense systems. In Asia-Pacific, surveillance drone swarms are prompting rapid countermeasure development, placing software-defined EW at the forefront of modernization plans.

Regional outlook

According to the report, North America remains the largest EW market, driven by significant US defense investment, strong domestic manufacturing, and robust R&D pipelines. While Canada and Mexico contribute modestly through modernization initiatives, reliance on imported gallium materials continues to pose a minor supply-chain risk. Asia-Pacific is emerging as the fastest-growing region. Expanding satellite programs, rising defense spending, and strategic collaborations—particularly among Japan, South Korea, India, and Australia—are boosting regional capabilities. Partnerships within frameworks like AUKUS are strengthening supply-chain diversity and supporting indigenous development as nations respond to ongoing maritime and territorial tensions.

If you enjoyed this article, you will like the following ones: don't miss them by subscribing to :

If you enjoyed this article, you will like the following ones: don't miss them by subscribing to :