Emerging technology in LED lighting to shape the outlook for 2014 predicts Yole

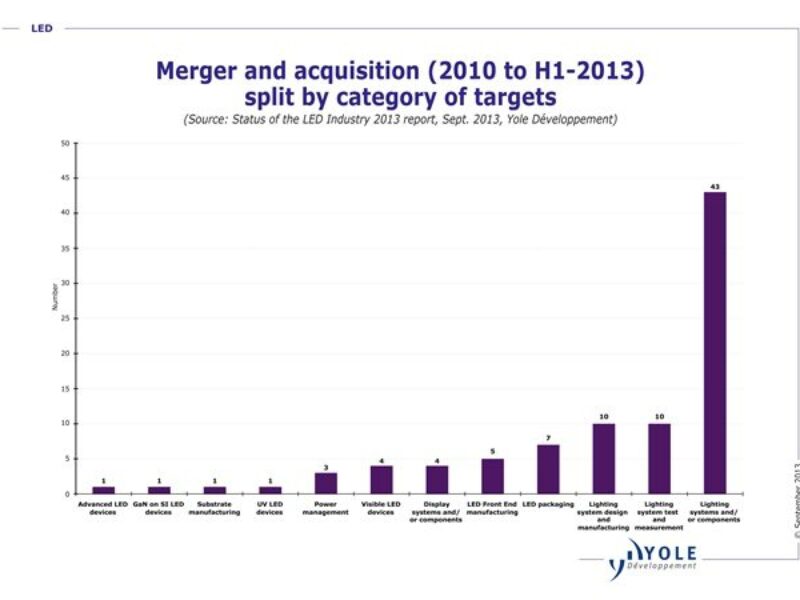

Mukish reckons that to successfully convert this opportunity into bottom line cash, the industry will have to undergo some major transformations, and many challenges await. First of all, the highly fragmented LED industry – with more than a hundred chip makers and thousands of packaging companies – needs some serious consolidations.

Secondly, the paradigm changes of SSL implied that it is no longer simply about making bulbs and sticking them into luminaires. To reap the full benefits of LEDs, products will have to be designed out of the box, almost from the chip to the final installation in our living room or city hall.

Developments toward technical innovation and manufacturing excellence both appear as mandatory conditions to continue to decrease the ‘$/lm’ of LED devices. However manufacturers should not focus only on reducing packaged LED costs, they should also decrease other component costs – such as IC drivers/power supplies, and optics – as light source cost reduction will reach its limit. Large incumbents like OSRAM and Philips have spent billions of dollars in acquisitions to evolve from light source manufacturers into full solution providers including light engines, luminaire controls.

"In 2013, LED technology has really started to spread beyond general lighting," explained Mukish. "With the LED penetration rate greater than 5% in some applications (such as residential lighting, commercial lighting and road and street lighting). However, to enable massive adoption of the technology, LED products still require a cost decrease in order to be able to compete with incumbent technologies (halogen…)".

Additionally, the switch from a display driven market to a Solid-State Lighting (SSL) driven market poses many challenges for the many LED manufacturers that are not vertically integrated all the way through to lamps/luminaires. Indeed, to address the LCD display market, LED manufacturers just needed to discuss with Samsung and LG (or, to be more specific, their backlighting unit suppliers, of which there are only a handful) and develop a few types of LEDs. With General Lighting, there are thousands of possible customers! The market is highly fragmented (in terms of applications and products). The channels to market have become much more complicated as they require a lot of commercial effort, and deal making with regional and local distributors.

Also, engineering gets requests to develop many different types of LEDs for each customer (one-chip package, multi-chip package, COB….). The segment becomes a ‘low volume/high product mix’ type of market without the benefit of commanding the usual high prices. The LED industry expects ‘low volume/high product mix’ products to still be priced like commodities. And to makes things harder, the only ‘large’ potential customers for SSL devices would be Philips Lighting, OSRAM and General Electric, but two of the three are vertically integrated and have their own source of LEDs that covers a large percentage of their needs.

With chip manufacturing being increasingly commoditized, it might be a matter of survival suggests Mukish. He believes winning companies will be the ones able to reach downstream, where most of the added value will lie. "Cree is the perfect example," explained Mukish. "The company has successfully evolved through the years from a material maker into a fully integrated SSL solution supplier. Even in Taiwan, leading chip maker Epistar has been reaching out downstream with an original strategy of virtual integration via partnerships and multiple cross-participations with system manufacturers".

Besides organization and rationalization, the industry must also educate all the stakeholders concludes Mukish. This means not only consumers but also architects, developers, light designers, and contractors. He spotlights one more challenge: while in many cases, government mandates to phase out inefficient lighting, this will leave the consumer with no other alternative than LED, so it would certainly help if LED lighting product manufacturers could offer more appealing products.

Visit Yole Développement at www.yole.fr

If you enjoyed this article, you will like the following ones: don't miss them by subscribing to :

If you enjoyed this article, you will like the following ones: don't miss them by subscribing to :