TrendForce: IC design houses see business decline in Q3

According tom the latest report from market watcher TrendForce, the revenue generation momentum of the global IC design industry slowed down in 3Q22.

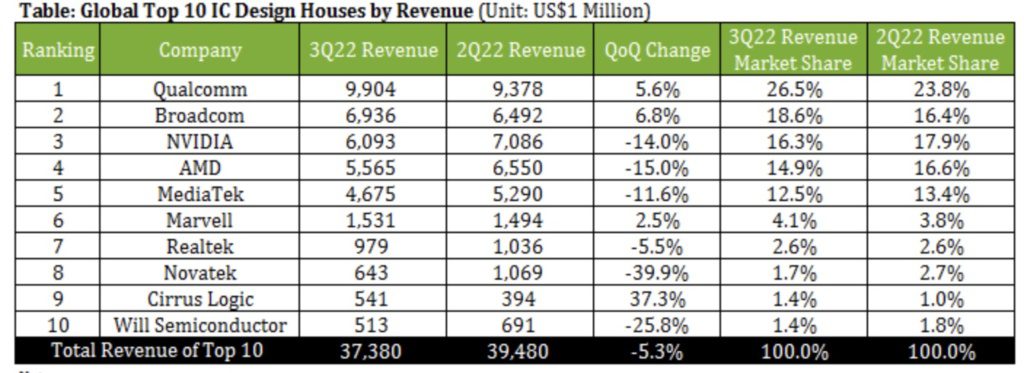

The main factors behind the decline were the Russia-Ukraine military conflict, the Covid-19 situation with exhaustive lockdowns in China, the ongoing inflation, and clients undergoing inventory corrections. The total revenue of the global top 10 IC design houses came to US$37.38 billion for 3Q22, showing a QoQ decline of 5.3%. Qualcomm remained first place in the ranking of the global top 10 IC design houses by revenue for 3Q22. Broadcom returned to second place by overtaking Nvidia and AMD, who slipped to third and fourth respectively due to weakening demand for PC graphic cards and cryptocurrency mining machines.

Regarding US-based IC design houses that were in the top 10 group for 3Q22, Qualcomm recorded a QoQ increase for the sales of smartphone SoCs and 5G modem chips. It also made gains in the automotive electronics market by expanding its collaborations with partners in the automotive industry. As a result, Qualcomm’s 3Q22 revenue figures for mobile and automotive offerings reflected QoQ increases of 6.8% and 22.0% respectively. The revenue growth of these two major product categories offset the marginal decline in the revenue for RF front-end chips. Qualcomm’s IC design revenue as a whole climbed up by 5.6% QoQ to US$9.90 billion for 3Q22. With such figures, the company sat firmly at the top of the ranking.

- Semiconductor market heads for biggest downturn since 2000

- WSTS lowers chip market forecast for 2022, 2023

Broadcom had a remarkable result for the sales of its semiconductor solutions in 3Q22. Thanks to the stable demand from the high-end segment of the market for networking devices, its revenue grew by 6.8% QoQ to US$6.94 billion. Broadcom’s acquisition of VMware is currently being reviewed by the relevant regulatory authorities. Once this deal is completed, Broadcom will have a chance to contend for the No. 1 spot in the revenue ranking, the report concludes.

Nvidia managed to raise sales for chips deployed in data centres and automotive electronics during 3Q22. However, these gains were not enough to compensate for the freeze in the demand for graphics cards equipped in cryptocurrency mining machines. Nvidia saw a QoQ drop of 32.6% in the revenue from solutions for gaming and a QoQ drop of 44.5% in the revenue from solutions for professional visualization. Under the bottom line, Nvidia posted a QoQ decline of 14.0% to US$6.09 billion.

© TrendForce

For 3Q22, AMD saw a QoQ increase of 8.3% in the revenue from businesses related to data centres. For the first time in AMD’s history, the revenue related to data centre solutions exceeded the revenue related client solutions (i.e., CPUs for desktops and laptops as well as other SoCs). Nevertheless, weakening demand for consumer electronics had a substantial impact on the revenue from client solutions, and this dragged down AMD’s overall performance. AMD posted a QoQ decline of 15.0% to US$5.57 billion.

Marvell was able to raise its 3Q22 revenue by 2.5% QoQ to US$1.53 billion because demand is relatively steady for its networking solutions (e.g., chips for data centres, enterprise network infrastructure, and automotive electronics). Turning to Cirrus Logic, it returned to the top 10 group in 3Q22 thanks to its lead in the market for low-power and high-precision mixed-signal processing solutions. Even though sales of Android smartphones were weak during that quarter, there was also an increase in the market penetration of certain audio chips for high-end Android smartphones. Moreover, Cirrus Logic benefited from an influx of Apple’s orders related to the new iPhone 14 series. Hence, its revenue rose by 37.3% QoQ to US$541 million in spite of the challenging market environment.

Consumer electronics slump hits Asian design houses

Among Taiwan-based IC design houses in the top 10 group for 3Q22, MediaTek posted a QoQ drop of 11.6% to US$4.68 billion. Due to Chinese smartphone brands’ weak sales performances and clients undergoing inventory corrections, MediaTek saw a QoQ decline in the revenues from mobile solutions, smart edge platforms, and power ICs. Inventory reduction will remain MediaTek’s top priority going forward. Turning to Realtek, sales of its solutions for networking and automotive applications remained stable in 3Q22. However, chips for PCs account for about 32% of its product mix, so the considerable shrinking of the demand for consumer electronics during the same period affected its overall performance. Realtek’s 3Q22 revenue came to US$979 million, showing a QoQ decline of 5.5%. As for Novatek, SoCs and display driver ICs as its two major product categories suffered a decline in both price and shipments. As a result, its 3Q22 revenue fell by 39.9% QoQ to US$643 million. Novatek experienced the steepest revenue drop among the top 10.

Will Semiconductor, which is based in Mainland China, posted a QoQ decline of 25.8% to US$513 million for 3Q22. Since the company mainly offers chips equipped in smartphones, its performance was affected by poor smartphone sales and Covid-19 lockdowns in China.

TrendForce points out that IC design houses have different product mix strategies. Therefore, demand has been steady for some them whose product mixes are mainly composed of solutions for data centres, networking hardware, IoT devices and automotive electronics. On the other hand, demand has weakened significantly for consumer electronics, display panels, and cryptocurrency mining machines, so the revenues from the related solutions have shrunk as well. Hence, the revenue results of the top 10 IC design houses for 3Q22 show gains for certain product categories coexisting with losses for others. Still, the semiconductor market as a whole has recently been in slump, so more than half of the top 10 posted a revenue decline for 3Q22.

Looking at the period from 4Q22 to 1Q23, TrendForce believes that because of the ongoing inflation, promotional activities related to the year-end holiday season will not lead to a significant rise in the overall demand for consumer electronics. Also, more time is needed to adjust inventory level for the demand side of the semiconductor market. Therefore, these two quarters are going to be very challenging for IC design houses, and the chance is high for them to post negative QoQ revenue results. However, IC design houses could also use this downturn period to lower their inventory levels while raising their cash levels. They could also introduce their products to other application segments, especially data centres and automotive electronics. In doing so, they would be better prepared for the future recovery of the whole semiconductor industry.

Related articles

Poor yield at Intel delays server processors, says TrendForce

Semiconductor market continues to fall

Foundry data shows the cracks in the semiconductor market

If you enjoyed this article, you will like the following ones: don't miss them by subscribing to :

If you enjoyed this article, you will like the following ones: don't miss them by subscribing to :